Colombia has positioned itself as a hotbed of fintech innovation in recent years. Do you want to know why? We will talk about the reasons for this and much more today in a new installment of Digitized Latin America, together with Americas Market Intelligence.

Digitization as a priority

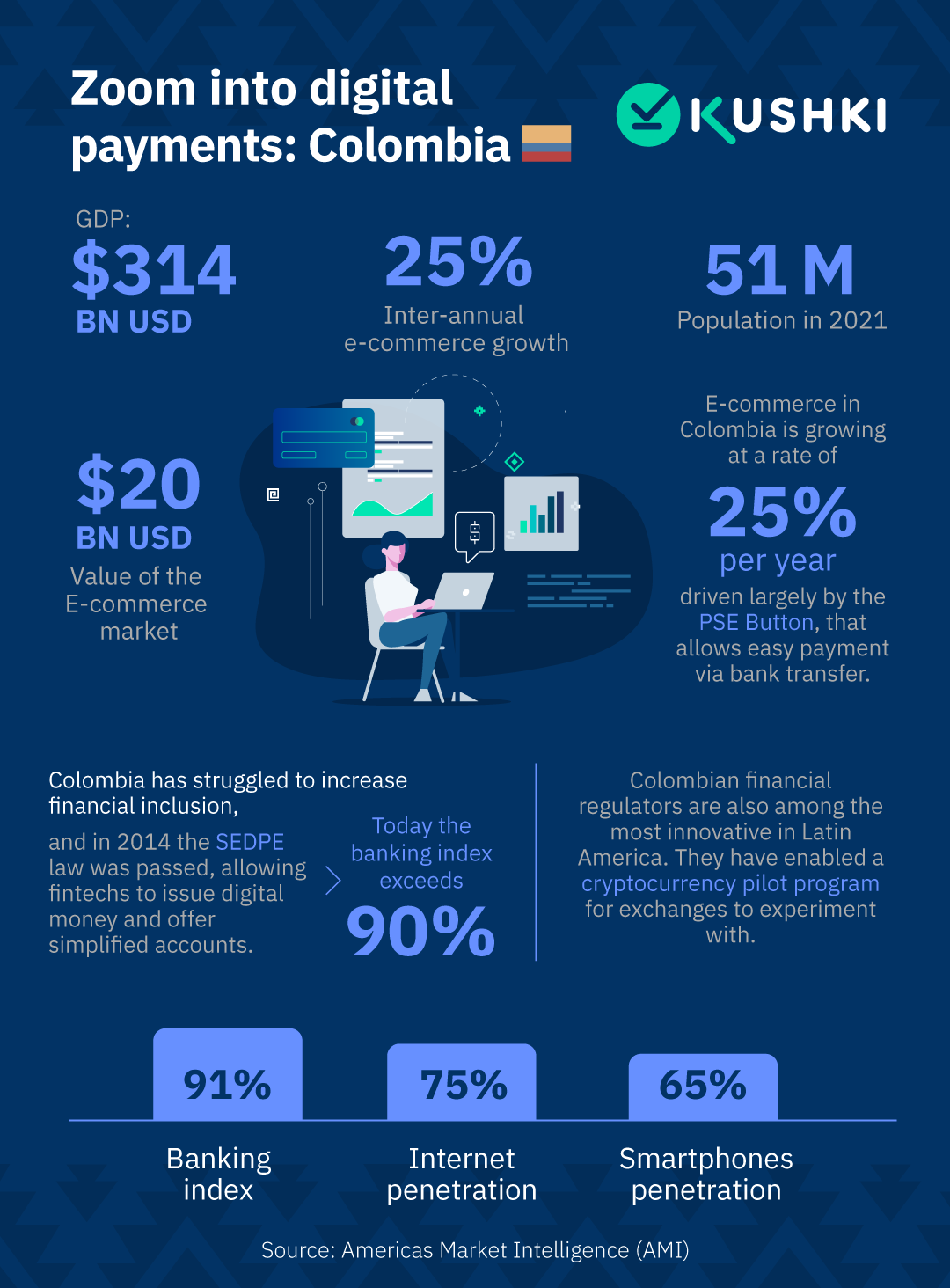

For several years, Colombia has been working to improve the financial inclusion of its population, which in 2021 reached 51 million people. In 2014, the SEDPE law was approved, which allows fintech companies to issue digital money and offer simplified accounts. With this regulation, financial inclusion has gradually increased over the years, and today the rate of access to banking services is over 90%.

Digital wallets also have an impressive share in Colombia, with 76% of the population using them. Super apps like DaviPlata, Nequi, or Movii enable public transport payments, social benefits, and even international remittances, among various other operations.

However, there is still a gap to work on in the country: internet access. Its mountainous geography means that only 26% of rural areas in Colombia have an internet connection. The government has taken on the task of solving this with three projects: Hogares Conectados, Navega TIC, and Zonas Digitales, which address aspects such as discounted internet rates, Wi-Fi access points, and the provision of free SIM cards.

E-commerce and new fintech models

Electronic commerce in Colombia has been growing at a rate of 25% per year, driven by the PSE button, an online payment button that allows a bank transfer as a payment method. The Colombian market has the highest share of bank transfers in payments for e-commerce, which demonstrates the need to implement other payment methods in addition to cards.

Regarding new models, in Colombia, the BNPL (Buy Now Pay Later) modality has been promoted with Addi, a company from that country that is gaining strength in this segment. The emergence of these companies is explained by the fact that Colombian financial regulators are among the most innovative in Latin America. For some years now, they have implemented a “crypto zone”, allowing cryptocurrency exchanges to experiment with deposit and withdrawal functionalities.

If you want to continue learning about digital payments in different countries of the region, review and subscribe to our blog.